Keysight Technologies (NYSE:KEYS) recently collaborated with AMD to advance PCI Express 6.0 technology, marking a significant step in high-speed data transfer and AI application development. Over the past quarter, the company experienced a 3% stock price increase, aligning closely with the market's modest gains. While the market has shown a 10% rise this year and anticipates 15% annual earnings growth, Keysight's performance was supported by its strong Q2 earnings and share buyback activities. These elements collectively reinforced the company's positive trajectory amid the broader market context, with no standout divergences from overall trends.

Rare earth metals are the new gold rush. Find out which 24 stocks are leading the charge.

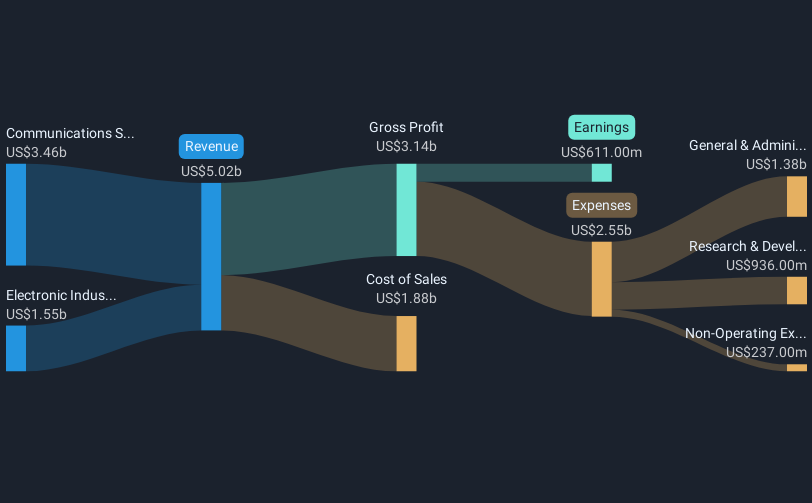

The collaboration between Keysight Technologies and AMD on PCI Express 6.0 technology could bolster revenue and earnings forecasts by enhancing the company's product offerings in high-speed data transfer and AI applications. This alignment with industry advancements is expected to strengthen Keysight's market position, potentially driving further growth in their software-centric and recurring revenue streams. As a result, this partnership may enhance the company's attractiveness to investors and improve its competitive edge in the evolving tech landscape.

Over the past five years, Keysight Technologies achieved a total return of 58.19%, reflecting consistent performance and resilience in a competitive market. This long-term gain provides context for the company's overall stock trajectory, supported by its strategic initiatives and diverse product portfolio. In contrast, during the past year, Keysight's return has outpaced the US Market, which generated a 9.8% rise, underscoring its robust positioning relative to industry peers.

The recent news could position Keysight to capitalize on growing demand in AI and data centers, potentially enhancing its revenue growth from the current 6% annual forecast. Moreover, aided by strategic acquisitions and collaboration, Keysight may experience improved margins and earnings stability. While its current share price of US$163.61 remains roughly 10.8% below the analyst consensus target of US$183.44, the emerging technology synergies may contribute positively towards closing this valuation gap. These developments could affirm analyst expectations if Keysight continues leveraging high-growth areas and optimizing its product mix.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com