The United States market has experienced a flat performance over the last week, but it has shown a 13% increase in the past year with earnings forecasted to grow by 14% annually. In this environment, identifying stocks that are potentially undervalued and have insider buying activity can be an effective strategy for investors looking to capitalize on growth opportunities.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Lindblad Expeditions Holdings | NA | 0.9x | 34.14% | ★★★★★★ |

| Five Star Bancorp | 12.3x | 4.7x | 46.48% | ★★★★★☆ |

| Columbus McKinnon | NA | 0.4x | 38.82% | ★★★★★☆ |

| Industrial Logistics Properties Trust | NA | 0.5x | 48.96% | ★★★★★☆ |

| Thryv Holdings | NA | 0.8x | 24.99% | ★★★★☆☆ |

| Titan Machinery | NA | 0.2x | -342.43% | ★★★★☆☆ |

| Farmland Partners | 9.2x | 9.3x | -20.36% | ★★★☆☆☆ |

| Delek US Holdings | NA | 0.1x | -56.84% | ★★★☆☆☆ |

| Tandem Diabetes Care | NA | 1.4x | -2751.65% | ★★★☆☆☆ |

| Montrose Environmental Group | NA | 1.0x | 5.22% | ★★★☆☆☆ |

We'll examine a selection from our screener results.

SolarEdge Technologies (NasdaqGS:SEDG)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: SolarEdge Technologies is a company that designs and manufactures solar energy solutions including inverters, power optimizers, and monitoring systems with a market cap of approximately $6.92 billion.

Operations: SolarEdge Technologies generates revenue primarily through its sales, with a notable trend in gross profit margin reaching 35.38% by the end of 2017 before declining to -87.07% by early 2025. The company's cost structure includes significant expenses in research and development, sales and marketing, and general administrative activities. Over time, operating expenses have increased alongside revenue growth but have not prevented fluctuations in net income margins.

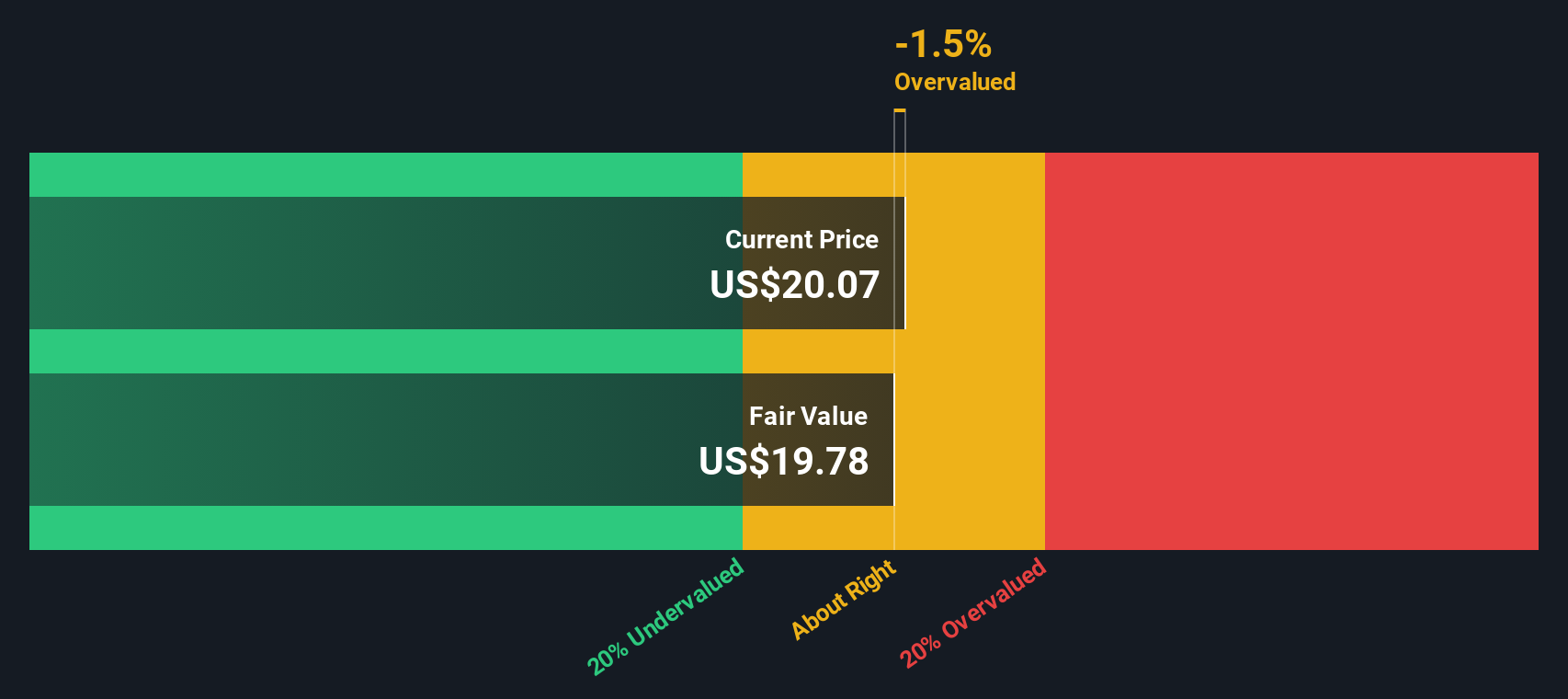

PE: -0.6x

SolarEdge Technologies, a smaller player in the U.S. market, is currently unprofitable and not expected to turn a profit over the next three years. Despite this, their revenue is projected to grow at 17.82% annually. Recent product launches like a solar-powered EV charging solution and strategic alliances for tax credit monetization highlight their innovation drive. With insider confidence shown through recent share purchases, SolarEdge's potential remains intriguing despite its volatile stock price and reliance on higher-risk funding sources.

- Click to explore a detailed breakdown of our findings in SolarEdge Technologies' valuation report.

Gain insights into SolarEdge Technologies' past trends and performance with our Past report.

Camping World Holdings (NYSE:CWH)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Camping World Holdings operates as a leading retailer specializing in recreational vehicles (RVs) and outdoor products, with additional services offered through its Good Sam brand, and has a market capitalization of approximately $1.77 billion.

Operations: Camping World Holdings generates revenue primarily from its RV and Outdoor Retail segment, complemented by Good Sam Services and Plans. The company's cost of goods sold (COGS) significantly impacts its gross profit, which has shown a varying trend with recent figures around 30.13%. Operating expenses, including general and administrative costs, are substantial components of the financial structure.

PE: -38.3x

Camping World Holdings, a smaller player in the market, is currently drawing attention for its potential value. Despite reporting a net loss of US$12.28 million in Q1 2025, an improvement from the previous year's US$22.31 million loss, insider confidence is evident through recent share purchases. The company has not diluted shares over the past year and anticipates earnings growth of 115% annually. A regular cash dividend was affirmed at US$0.125 per share, signaling stability amidst financial challenges and higher-risk funding sources reliant on external borrowing rather than customer deposits.

- Click here to discover the nuances of Camping World Holdings with our detailed analytical valuation report.

Explore historical data to track Camping World Holdings' performance over time in our Past section.

Vishay Intertechnology (NYSE:VSH)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Vishay Intertechnology is a global manufacturer of discrete semiconductors and passive electronic components, with operations spanning diodes, MOSFETs, inductors, resistors, capacitors, and optoelectronic components.

Operations: Vishay Intertechnology's revenue streams are primarily derived from its product segments, with resistors and MOSFETs being significant contributors. The company has experienced fluctuations in its gross profit margin, peaking at 30.87% in early 2023 before declining to 20.35% by mid-2025. Operating expenses have generally increased over time, impacting the overall profitability of the business.

PE: -30.3x

Vishay Intertechnology, a key player in the semiconductor and passive electronic components market, recently launched innovative products like the SiEH4800EW MOSFET and D2TO35H resistor, enhancing efficiency and reliability across various applications. Despite reporting a net loss of US$4.09 million for Q1 2025 compared to last year's profit, insider confidence remains strong with significant share repurchases totaling 728,560 shares between January and March 2025. The company's focus on cutting-edge technology positions it well for future growth in sectors like automotive and industrial markets.

- Delve into the full analysis valuation report here for a deeper understanding of Vishay Intertechnology.

Assess Vishay Intertechnology's past performance with our detailed historical performance reports.

Where To Now?

- Click here to access our complete index of 110 Undervalued US Small Caps With Insider Buying.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com