Prenetics Global Limited (NASDAQ:PRE) shares have had a really impressive month, gaining 50% after a shaky period beforehand. But the gains over the last month weren't enough to make shareholders whole, as the share price is still down 9.0% in the last twelve months.

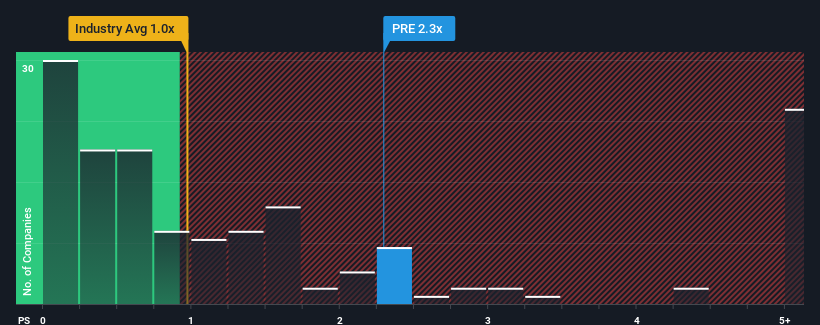

Since its price has surged higher, given close to half the companies operating in the United States' Healthcare industry have price-to-sales ratios (or "P/S") below 1x, you may consider Prenetics Global as a stock to potentially avoid with its 2.3x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

Check out our latest analysis for Prenetics Global

How Has Prenetics Global Performed Recently?

Recent times have been advantageous for Prenetics Global as its revenues have been rising faster than most other companies. It seems that many are expecting the strong revenue performance to persist, which has raised the P/S. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Keen to find out how analysts think Prenetics Global's future stacks up against the industry? In that case, our free report is a great place to start.How Is Prenetics Global's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as high as Prenetics Global's is when the company's growth is on track to outshine the industry.

Taking a look back first, we see that the company grew revenue by an impressive 41% last year. The latest three year period has also seen an excellent 144% overall rise in revenue, aided by its short-term performance. So we can start by confirming that the company has done a great job of growing revenue over that time.

Turning to the outlook, the next year should generate growth of 158% as estimated by the only analyst watching the company. With the industry only predicted to deliver 9.2%, the company is positioned for a stronger revenue result.

In light of this, it's understandable that Prenetics Global's P/S sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Final Word

Prenetics Global shares have taken a big step in a northerly direction, but its P/S is elevated as a result. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Prenetics Global maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Healthcare industry, as expected. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. Unless these conditions change, they will continue to provide strong support to the share price.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Prenetics Global you should know about.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.