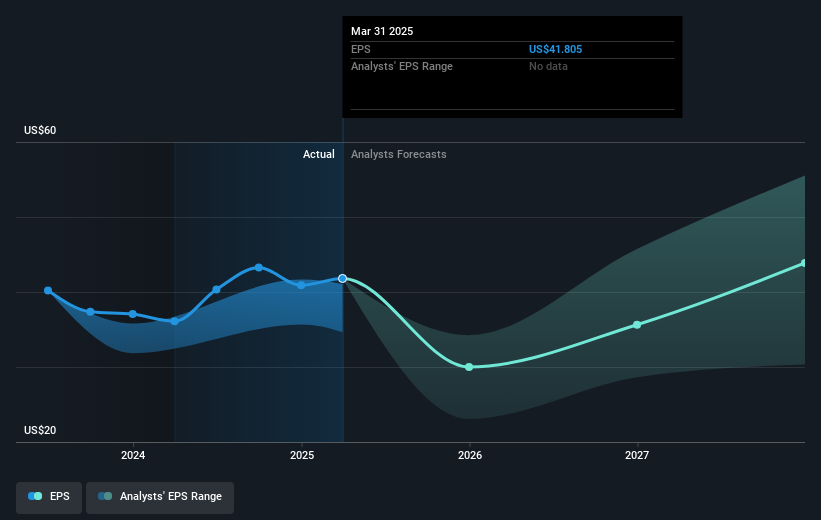

Regeneron Pharmaceuticals (NasdaqGS:REGN) recently reported earnings for Q1 2025 with a revenue drop to $3,029 million compared to the prior year, though net income increased, reflecting robust profitability with diluted earnings per share rising to $7.27. The company declared a dividend and executed a significant share repurchase. Despite these positive financial maneuvers, the stock dropped by 8.5% over the last month. Factors like the FDA's complete response letter for EYLEA HD and the broader market's flat performance may have added weight to this decline while the market climbed 8% over the past year.

The recent 8.5% decline in Regeneron Pharmaceuticals' share price contrasts with the broader market performance and may reflect investor concerns about near-term hurdles like the FDA's complete response letter for EYLEA HD. These issues could temporarily pressure revenue and earnings forecasts if product approvals are delayed or market competition increases. Despite this, the company's strategic investments in manufacturing and R&D aim to support long-term growth through expansion of its core drug franchises and introduction of new therapies.

In a longer-term context, Regeneron's total shareholder return, including dividends, was a decline of 8.37% over the past five years. This performance trails the past year's market return of 8% and the biotech industry's 15.2% decline, illustrating challenges in maintaining growth in a competitive sector. Analysts' consensus price target of US$800.13 suggests a potential upside from the current share price of US$558.52, although investor perception may differ due to external pressures on key products. The focus remains on expanding global commercialization and leveraging pipeline innovations to enhance future revenue and earnings performance.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com