As the U.S. market experiences a surge driven by new trade deals and optimism surrounding future agreements, investors are keenly observing opportunities that may arise from these developments. In such an environment, identifying stocks that are potentially undervalued can be crucial for those looking to capitalize on discrepancies between market price and intrinsic value, especially when market conditions suggest room for growth or recovery.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Atour Lifestyle Holdings (NasdaqGS:ATAT) | $26.59 | $51.85 | 48.7% |

| MetroCity Bankshares (NasdaqGS:MCBS) | $28.17 | $55.08 | 48.9% |

| Super Group (SGHC) (NYSE:SGHC) | $9.07 | $18.05 | 49.8% |

| German American Bancorp (NasdaqGS:GABC) | $38.43 | $74.67 | 48.5% |

| DoorDash (NasdaqGS:DASH) | $176.99 | $353.76 | 50% |

| Ready Capital (NYSE:RC) | $4.41 | $8.67 | 49.1% |

| Pure Storage (NYSE:PSTG) | $47.64 | $93.60 | 49.1% |

| Amerant Bancorp (NYSE:AMTB) | $17.28 | $33.41 | 48.3% |

| HealthEquity (NasdaqGS:HQY) | $91.72 | $179.14 | 48.8% |

| Nutanix (NasdaqGS:NTNX) | $73.70 | $145.75 | 49.4% |

We're going to check out a few of the best picks from our screener tool.

First Advantage (NasdaqGS:FA)

Overview: First Advantage Corporation offers employment background screening and identity verification solutions globally, with a market cap of approximately $2.57 billion.

Operations: First Advantage Corporation's revenue segments include employment background screening and identity verification solutions, with a focus on providing these services worldwide.

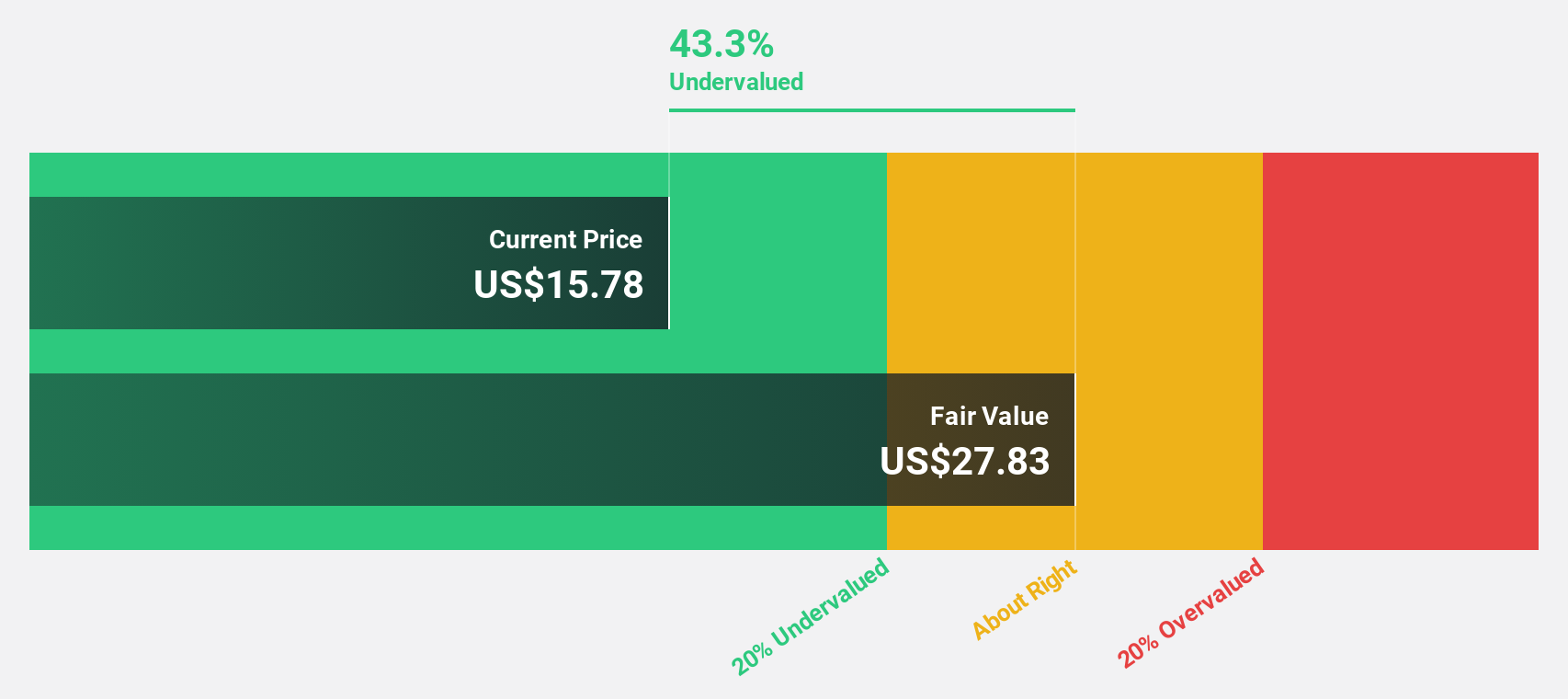

Estimated Discount To Fair Value: 45.6%

First Advantage is trading at US$14.97, significantly below its estimated fair value of US$27.53, indicating potential undervaluation based on cash flows. Despite a recent net loss of US$41.19 million for Q1 2025, the company expects revenue growth between US$1.5 billion and US$1.6 billion for the year, with annual revenue forecasted to grow at 22.7%, surpassing market averages and signaling strong future cash flow prospects despite current profitability challenges.

- Our expertly prepared growth report on First Advantage implies its future financial outlook may be stronger than recent results.

- Navigate through the intricacies of First Advantage with our comprehensive financial health report here.

Flywire (NasdaqGS:FLYW)

Overview: Flywire Corporation operates as a payments enablement and software company both in the United States and internationally, with a market cap of approximately $1.22 billion.

Operations: Flywire generates revenue through its operations as a payments enablement and software company, serving clients both domestically and globally.

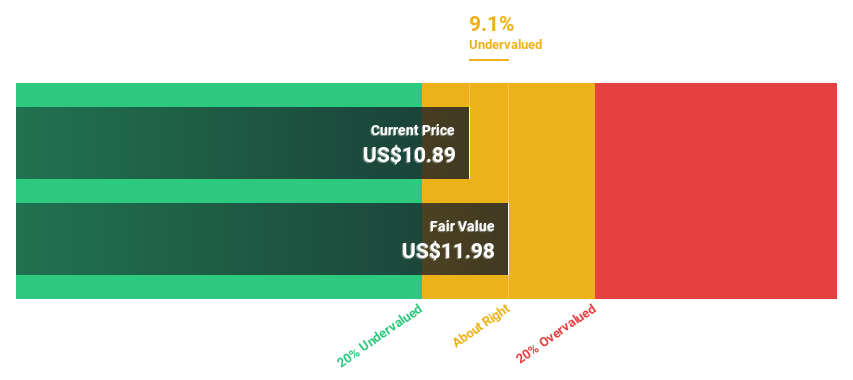

Estimated Discount To Fair Value: 20.2%

Flywire, currently priced at US$10.9, is trading below its estimated fair value of US$13.66, suggesting it may be undervalued based on cash flows. The company recently reported Q1 2025 sales of US$133.45 million and reduced its net loss to US$4.16 million from the previous year. With revenue growth expected at 13.2% annually and earnings projected to grow significantly above market averages, Flywire shows promising potential despite recent volatility in share price.

- In light of our recent growth report, it seems possible that Flywire's financial performance will exceed current levels.

- Get an in-depth perspective on Flywire's balance sheet by reading our health report here.

OneMain Holdings (NYSE:OMF)

Overview: OneMain Holdings, Inc. is a financial services holding company that operates in the consumer finance and insurance sectors across the United States, with a market cap of approximately $5.76 billion.

Operations: The company's revenue is primarily derived from its consumer and insurance operations, generating $2.57 billion.

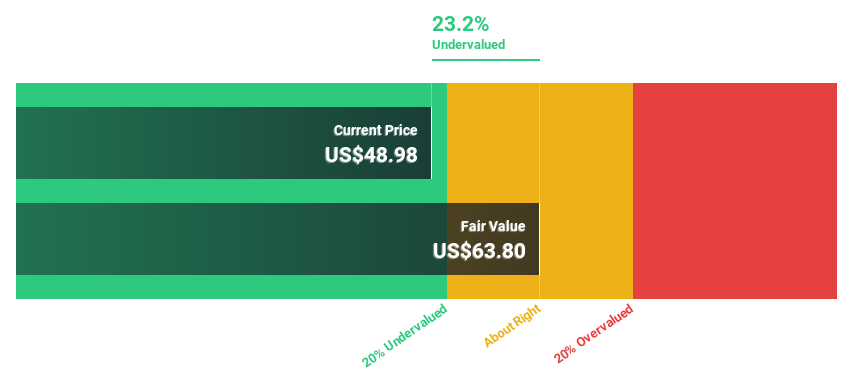

Estimated Discount To Fair Value: 23.7%

OneMain Holdings, priced at US$48.7, trades below its fair value estimate of US$63.8, highlighting potential undervaluation based on cash flows. Despite significant insider selling and net charge-offs rising to US$473 million, earnings are projected to grow 25.06% annually, outpacing the market's growth rate. Recent Q1 results showed net income increasing to US$213 million from the previous year, with revenue expected to rise by up to 8% for 2025 amidst ongoing share repurchases.

- Upon reviewing our latest growth report, OneMain Holdings' projected financial performance appears quite optimistic.

- Unlock comprehensive insights into our analysis of OneMain Holdings stock in this financial health report.

Key Takeaways

- Click here to access our complete index of 174 Undervalued US Stocks Based On Cash Flows.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com