Lonking Holdings (HKG:3339) Full Year 2024 Results

Key Financial Results

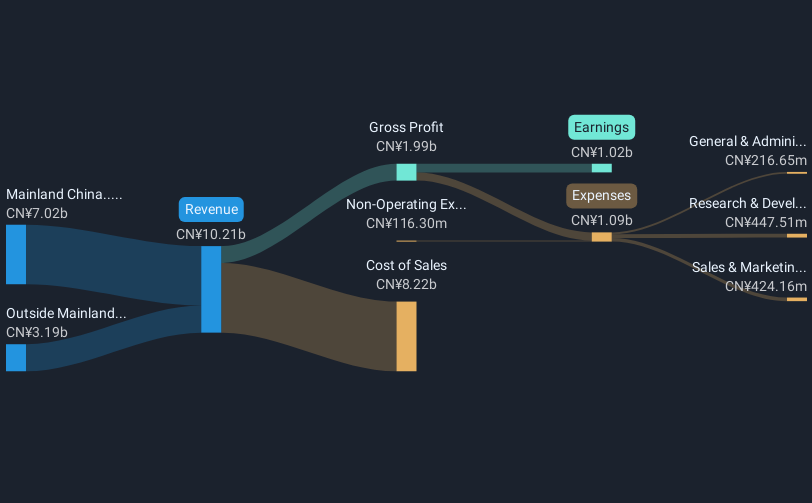

- Revenue: CN¥10.2b (down 2.9% from FY 2023).

- Net income: CN¥1.02b (up 58% from FY 2023).

- Profit margin: 10.0% (up from 6.1% in FY 2023). The increase in margin was driven by lower expenses.

- EPS: CN¥0.24 (up from CN¥0.15 in FY 2023).

All figures shown in the chart above are for the trailing 12 month (TTM) period

Lonking Holdings EPS Beats Expectations, Revenues Fall Short

Revenue missed analyst estimates by 5.3%. Earnings per share (EPS) exceeded analyst estimates by 32%.

The primary driver behind last 12 months revenue was the Mainland China segment contributing a total revenue of CN¥7.02b (69% of total revenue). Notably, cost of sales worth CN¥8.22b amounted to 81% of total revenue thereby underscoring the impact on earnings. The largest operating expense was Research & Development (R&D) costs, amounting to CN¥447.5m (41% of total expenses). Over the last 12 months, the company's earnings were enhanced by non-operating gains of CN¥116.3m. Explore how 3339's revenue and expenses shape its earnings.

Looking ahead, revenue is forecast to grow 7.6% p.a. on average during the next 3 years, compared to a 13% growth forecast for the Machinery industry in Hong Kong.

Performance of the Hong Kong Machinery industry.

The company's share price is broadly unchanged from a week ago.

Risk Analysis

Be aware that Lonking Holdings is showing 1 warning sign in our investment analysis that you should know about...

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.