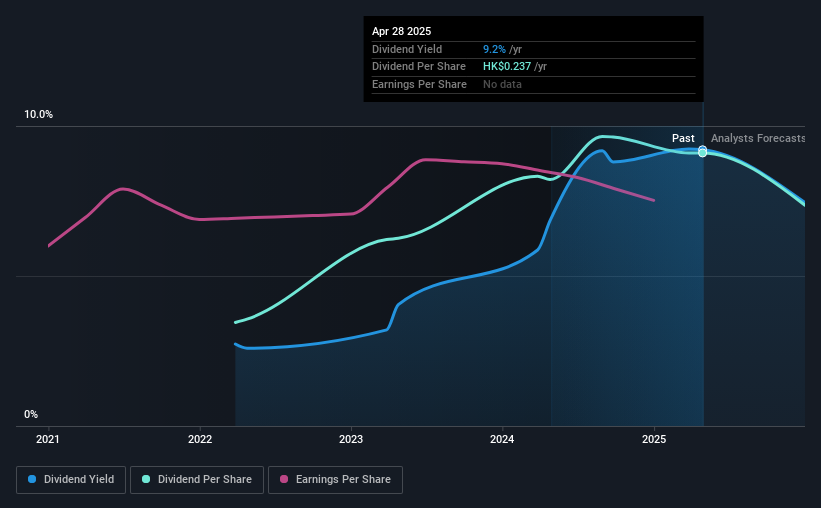

Chaoju Eye Care Holdings Limited (HKG:2219) is reducing its dividend from last year's comparable payment to CN¥0.1193 on the 27th of June. The dividend yield of 9.2% is still a nice boost to shareholder returns, despite the cut.

Chaoju Eye Care Holdings' Projected Earnings Seem Likely To Cover Future Distributions

A big dividend yield for a few years doesn't mean much if it can't be sustained. Before this announcement, Chaoju Eye Care Holdings was paying out 83% of earnings, but a comparatively small 43% of free cash flows. This leaves plenty of cash for reinvestment into the business.

Looking forward, earnings per share is forecast to rise by 30.7% over the next year. Under the assumption that the dividend will continue along recent trends, we think the payout ratio could be 68% which would be quite comfortable going to take the dividend forward.

View our latest analysis for Chaoju Eye Care Holdings

Chaoju Eye Care Holdings Doesn't Have A Long Payment History

The dividend has been pretty stable looking back, but the company hasn't been paying one for very long. This makes it tough to judge how it would fare through a full economic cycle. The dividend has gone from an annual total of CN¥0.0844 in 2022 to the most recent total annual payment of CN¥0.223. This works out to be a compound annual growth rate (CAGR) of approximately 38% a year over that time. It is always nice to see strong dividend growth, but with such a short payment history we wouldn't be inclined to rely on it until a longer track record can be developed.

The Dividend's Growth Prospects Are Limited

Investors could be attracted to the stock based on the quality of its payment history. Earnings have grown at around 2.9% a year for the past three years, which isn't massive but still better than seeing them shrink. Chaoju Eye Care Holdings' earnings per share has barely grown, which is not ideal - perhaps this is why the company pays out the majority of its earnings to shareholders. This isn't the end of the world, but for investors looking for strong dividend growth they may want to look elsewhere.

Our Thoughts On Chaoju Eye Care Holdings' Dividend

Overall, it's not great to see that the dividend has been cut, but this might be explained by the payments being a bit high previously. The payments haven't been particularly stable and we don't see huge growth potential, but with the dividend well covered by cash flows it could prove to be reliable over the short term. We would be a touch cautious of relying on this stock primarily for the dividend income.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. See if management have their own wealth at stake, by checking insider shareholdings in Chaoju Eye Care Holdings stock. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.