Key Insights

- Xtep International Holdings' Annual General Meeting to take place on 28th of April

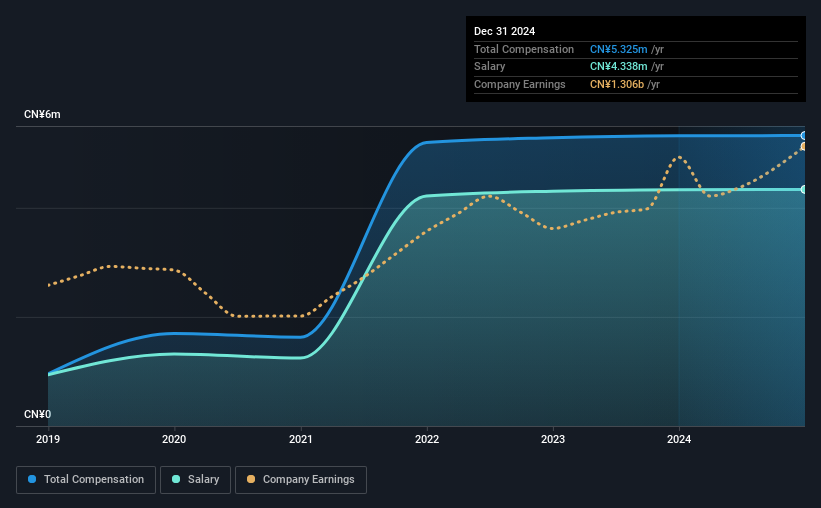

- Salary of CN¥4.34m is part of CEO Shui Po Ding's total remuneration

- Total compensation is similar to the industry average

- Xtep International Holdings' three-year loss to shareholders was 44% while its EPS grew by 10% over the past three years

The underwhelming share price performance of Xtep International Holdings Limited (HKG:1368) in the past three years would have disappointed many shareholders. However, what is unusual is that EPS growth has been positive, suggesting that the share price has diverged from fundamentals. Shareholders may want to question the board on the future direction of the company at the upcoming AGM on 28th of April. Voting on resolutions such as executive remuneration and other matters could also be a way to influence management. We discuss below why we think shareholders should be cautious of approving a raise for the CEO at the moment.

View our latest analysis for Xtep International Holdings

How Does Total Compensation For Shui Po Ding Compare With Other Companies In The Industry?

At the time of writing, our data shows that Xtep International Holdings Limited has a market capitalization of HK$13b, and reported total annual CEO compensation of CN¥5.3m for the year to December 2024. That is, the compensation was roughly the same as last year. In particular, the salary of CN¥4.34m, makes up a huge portion of the total compensation being paid to the CEO.

For comparison, other companies in the Hong Kong Luxury industry with market capitalizations ranging between HK$7.8b and HK$25b had a median total CEO compensation of CN¥5.3m. So it looks like Xtep International Holdings compensates Shui Po Ding in line with the median for the industry. Furthermore, Shui Po Ding directly owns HK$353m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | CN¥4.3m | CN¥4.3m | 81% |

| Other | CN¥987k | CN¥987k | 19% |

| Total Compensation | CN¥5.3m | CN¥5.3m | 100% |

Talking in terms of the industry, salary represented approximately 86% of total compensation out of all the companies we analyzed, while other remuneration made up 14% of the pie. Xtep International Holdings is largely mirroring the industry average when it comes to the share a salary enjoys in overall compensation. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at Xtep International Holdings Limited's Growth Numbers

Over the past three years, Xtep International Holdings Limited has seen its earnings per share (EPS) grow by 10% per year. It achieved revenue growth of 6.5% over the last year.

Shareholders would be glad to know that the company has improved itself over the last few years. It's also good to see modest revenue growth, suggesting the underlying business is healthy. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Xtep International Holdings Limited Been A Good Investment?

The return of -44% over three years would not have pleased Xtep International Holdings Limited shareholders. So shareholders would probably want the company to be less generous with CEO compensation.

To Conclude...

The fact that shareholders are sitting on a loss on the value of their shares in the past few years is certainly disconcerting. The stock's movement is disjointed with the company's earnings growth, which ideally should move in the same direction. Shareholders would probably be keen to find out what are the other factors could be weighing down the stock. The upcoming AGM will be a chance for shareholders to question the board on key matters, such as CEO remuneration or any other issues they might have and revisit their investment thesis with regards to the company.

CEO compensation can have a massive impact on performance, but it's just one element. That's why we did some digging and identified 1 warning sign for Xtep International Holdings that investors should think about before committing capital to this stock.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.