Shareholders didn't seem to be thrilled with Medlive Technology Co., Ltd.'s (HKG:2192) recent earnings report, despite healthy profit numbers. Our analysis suggests they may be concerned about some underlying details.

Examining Cashflow Against Medlive Technology's Earnings

In high finance, the key ratio used to measure how well a company converts reported profits into free cash flow (FCF) is the accrual ratio (from cashflow). The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. That is not intended to imply we should worry about a positive accrual ratio, but it's worth noting where the accrual ratio is rather high. To quote a 2014 paper by Lewellen and Resutek, "firms with higher accruals tend to be less profitable in the future".

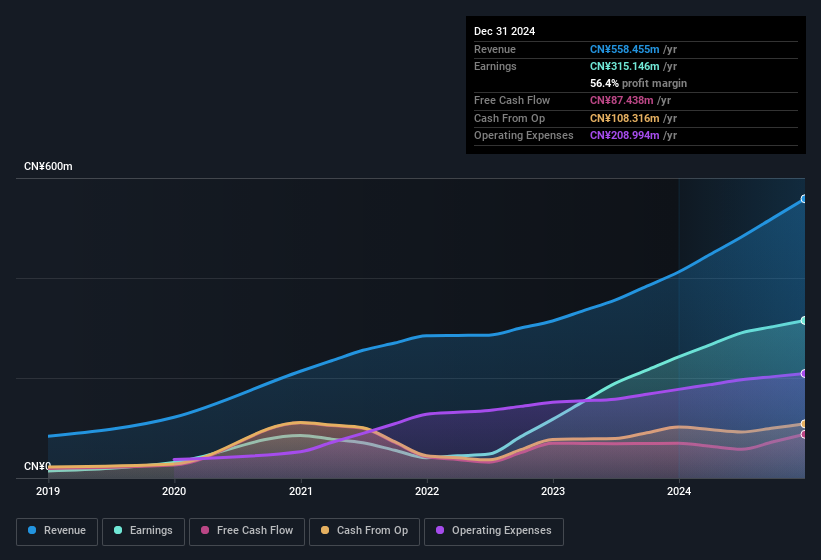

Medlive Technology has an accrual ratio of 0.48 for the year to December 2024. Ergo, its free cash flow is significantly weaker than its profit. As a general rule, that bodes poorly for future profitability. To wit, it produced free cash flow of CN¥87m during the period, falling well short of its reported profit of CN¥315.1m. We note, however, that Medlive Technology grew its free cash flow over the last year. However, that's not all there is to consider. We can see that unusual items have impacted its statutory profit, and therefore the accrual ratio.

View our latest analysis for Medlive Technology

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

The Impact Of Unusual Items On Profit

Given the accrual ratio, it's not overly surprising that Medlive Technology's profit was boosted by unusual items worth CN¥9.1m in the last twelve months. While we like to see profit increases, we tend to be a little more cautious when unusual items have made a big contribution. When we crunched the numbers on thousands of publicly listed companies, we found that a boost from unusual items in a given year is often not repeated the next year. And, after all, that's exactly what the accounting terminology implies. If Medlive Technology doesn't see that contribution repeat, then all else being equal we'd expect its profit to drop over the current year.

Our Take On Medlive Technology's Profit Performance

Summing up, Medlive Technology received a nice boost to profit from unusual items, but could not match its paper profit with free cash flow. For the reasons mentioned above, we think that a perfunctory glance at Medlive Technology's statutory profits might make it look better than it really is on an underlying level. So while earnings quality is important, it's equally important to consider the risks facing Medlive Technology at this point in time. For example, we've found that Medlive Technology has 2 warning signs (1 doesn't sit too well with us!) that deserve your attention before going any further with your analysis.

Our examination of Medlive Technology has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.