Best Pacific International Holdings Limited (HKG:2111) shareholders that were waiting for something to happen have been dealt a blow with a 36% share price drop in the last month. Looking at the bigger picture, even after this poor month the stock is up 32% in the last year.

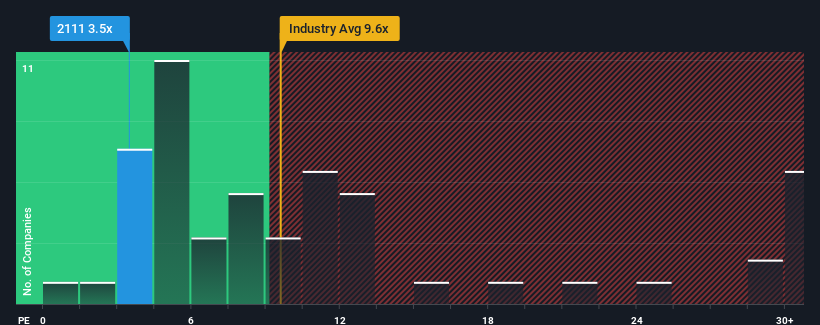

Even after such a large drop in price, Best Pacific International Holdings' price-to-earnings (or "P/E") ratio of 3.5x might still make it look like a strong buy right now compared to the market in Hong Kong, where around half of the companies have P/E ratios above 11x and even P/E's above 22x are quite common. However, the P/E might be quite low for a reason and it requires further investigation to determine if it's justified.

Best Pacific International Holdings certainly has been doing a good job lately as it's been growing earnings more than most other companies. One possibility is that the P/E is low because investors think this strong earnings performance might be less impressive moving forward. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Best Pacific International Holdings

Is There Any Growth For Best Pacific International Holdings?

In order to justify its P/E ratio, Best Pacific International Holdings would need to produce anemic growth that's substantially trailing the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 75% last year. The latest three year period has also seen an excellent 51% overall rise in EPS, aided by its short-term performance. So we can start by confirming that the company has done a great job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 14% per annum during the coming three years according to the only analyst following the company. That's shaping up to be similar to the 14% per annum growth forecast for the broader market.

In light of this, it's peculiar that Best Pacific International Holdings' P/E sits below the majority of other companies. It may be that most investors are not convinced the company can achieve future growth expectations.

The Final Word

Having almost fallen off a cliff, Best Pacific International Holdings' share price has pulled its P/E way down as well. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our examination of Best Pacific International Holdings' analyst forecasts revealed that its market-matching earnings outlook isn't contributing to its P/E as much as we would have predicted. When we see an average earnings outlook with market-like growth, we assume potential risks are what might be placing pressure on the P/E ratio. It appears some are indeed anticipating earnings instability, because these conditions should normally provide more support to the share price.

And what about other risks? Every company has them, and we've spotted 1 warning sign for Best Pacific International Holdings you should know about.

You might be able to find a better investment than Best Pacific International Holdings. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.