Key Insights

- Gemilang International will host its Annual General Meeting on 14th of March

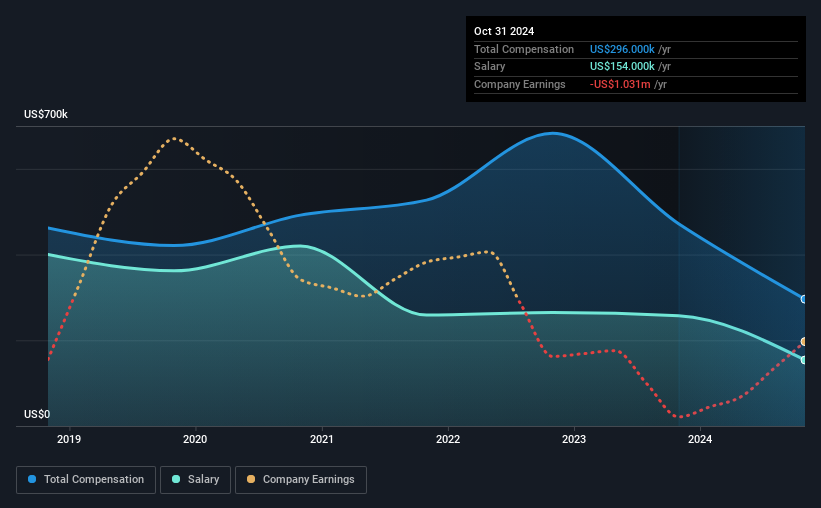

- Salary of US$154.0k is part of CEO Chong Yong Pang's total remuneration

- The overall pay is comparable to the industry average

- Gemilang International's three-year loss to shareholders was 69% while its EPS was down 72% over the past three years

Shareholders of Gemilang International Limited (HKG:6163) will have been dismayed by the negative share price return over the last three years. Per share earnings growth is also poor, despite revenues growing. Shareholders will have a chance to take their concerns to the board at the next AGM on 14th of March and vote on resolutions including executive compensation, which studies show may have an impact on company performance. We think shareholders may be cautious of approving a pay rise for the CEO at the moment, based on our analysis below.

Check out our latest analysis for Gemilang International

How Does Total Compensation For Chong Yong Pang Compare With Other Companies In The Industry?

At the time of writing, our data shows that Gemilang International Limited has a market capitalization of HK$50m, and reported total annual CEO compensation of US$296k for the year to October 2024. Notably, that's a decrease of 37% over the year before. Notably, the salary which is US$154.0k, represents a considerable chunk of the total compensation being paid.

On comparing similar-sized companies in the Hong Kong Machinery industry with market capitalizations below HK$1.6b, we found that the median total CEO compensation was US$296k. So it looks like Gemilang International compensates Chong Yong Pang in line with the median for the industry. Furthermore, Chong Yong Pang directly owns HK$18m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | US$154k | US$257k | 52% |

| Other | US$142k | US$215k | 48% |

| Total Compensation | US$296k | US$472k | 100% |

Talking in terms of the industry, salary represented approximately 77% of total compensation out of all the companies we analyzed, while other remuneration made up 23% of the pie. Gemilang International sets aside a smaller share of compensation for salary, in comparison to the overall industry. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at Gemilang International Limited's Growth Numbers

Gemilang International Limited has reduced its earnings per share by 72% a year over the last three years. Its revenue is up 61% over the last year.

The reduction in EPS, over three years, is arguably concerning. But on the other hand, revenue growth is strong, suggesting a brighter future. In conclusion we can't form a strong opinion about business performance yet; but it's one worth watching. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Gemilang International Limited Been A Good Investment?

Few Gemilang International Limited shareholders would feel satisfied with the return of -69% over three years. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

To Conclude...

The returns to shareholders is disappointing along with lack of earnings growth, which goes some way in explaining the poor returns. Shareholders will get the chance at the upcoming AGM to question the board on key matters, such as CEO remuneration or any other issues they might have and revisit their investment thesis with regards to the company.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. We've identified 3 warning signs for Gemilang International that investors should be aware of in a dynamic business environment.

Important note: Gemilang International is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.