Amid geopolitical tensions and tariff concerns, Asian markets have shown resilience, with China's tech sector experiencing a notable uplift due to strong earnings reports. In such an environment, identifying undervalued stocks can be crucial for investors seeking opportunities; these stocks are often priced below their intrinsic value, offering potential for growth as market conditions stabilize.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Guangdong Fenghua Advanced Technology (Holding) (SZSE:000636) | CN¥15.16 | CN¥30.21 | 49.8% |

| Power Wind Health Industry (TWSE:8462) | NT$112.00 | NT$223.88 | 50% |

| Aoshikang Technology (SZSE:002913) | CN¥29.20 | CN¥58.34 | 50% |

| Samyang Foods (KOSE:A003230) | ₩884000.00 | ₩1721951.23 | 48.7% |

| Food & Life Companies (TSE:3563) | ¥4052.00 | ¥8096.60 | 50% |

| LITALICO (TSE:7366) | ¥1090.00 | ¥2149.14 | 49.3% |

| Sung Kwang BendLtd (KOSDAQ:A014620) | ₩28200.00 | ₩55950.78 | 49.6% |

| Nanjing King-Friend Biochemical PharmaceuticalLtd (SHSE:603707) | CN¥12.72 | CN¥24.90 | 48.9% |

| BalnibarbiLtd (TSE:3418) | ¥1069.00 | ¥2085.86 | 48.8% |

| Shenzhen Dynanonic (SZSE:300769) | CN¥39.04 | CN¥77.10 | 49.4% |

Here we highlight a subset of our preferred stocks from the screener.

Shenzhou International Group Holdings (SEHK:2313)

Overview: Shenzhou International Group Holdings Limited is an investment holding company involved in the manufacture, printing, and sale of knitwear products across Mainland China, the European Union, the United States, Japan, and other international markets with a market cap of approximately HK$89.14 billion.

Operations: The company's revenue primarily stems from its manufacture and sale of knitwear products, totaling approximately CN¥26.38 billion.

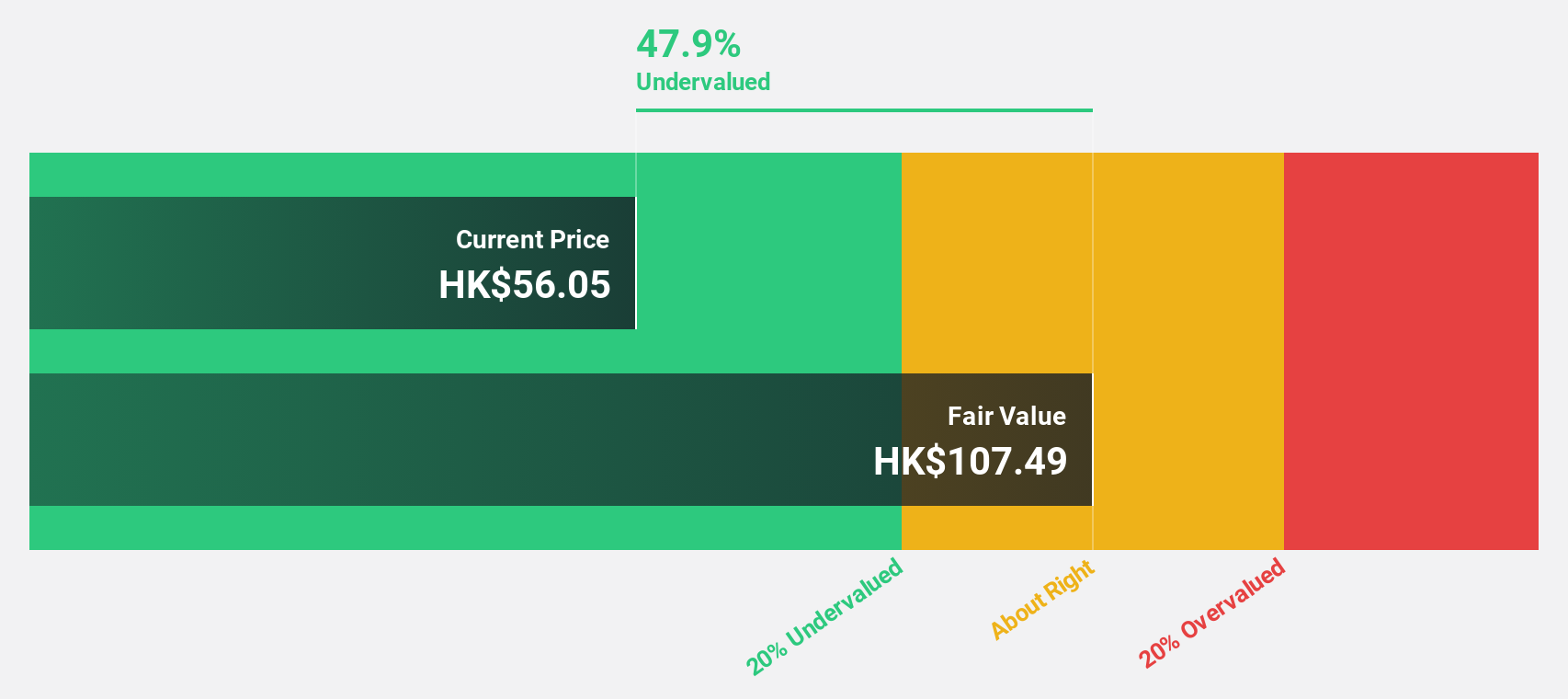

Estimated Discount To Fair Value: 48.2%

Shenzhou International Group Holdings is trading at HK$59.3, significantly below its estimated fair value of HK$114.53, presenting a potential undervaluation based on cash flows. Revenue growth is forecasted at 10.7% annually, outpacing the Hong Kong market's 8%. Although earnings are expected to grow by 12.54% yearly, they remain below significant thresholds but still surpass market averages. Analysts anticipate a stock price increase of over 50%, despite an unstable dividend history.

- The growth report we've compiled suggests that Shenzhou International Group Holdings' future prospects could be on the up.

- Click to explore a detailed breakdown of our findings in Shenzhou International Group Holdings' balance sheet health report.

Smoore International Holdings (SEHK:6969)

Overview: Smoore International Holdings Limited is an investment holding company that provides vaping technology solutions, with a market cap of HK$76.65 billion.

Operations: Smoore International Holdings Limited generates its revenue primarily through the provision of vaping technology solutions.

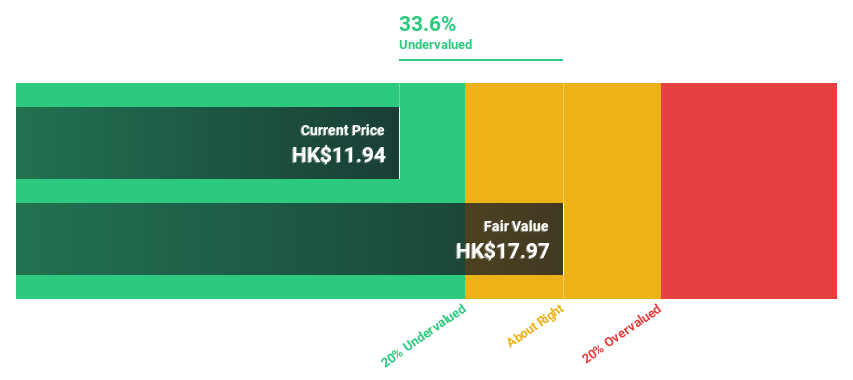

Estimated Discount To Fair Value: 30.5%

Smoore International Holdings, trading at HK$12.4, is undervalued relative to its estimated fair value of HK$17.83, suggesting potential based on cash flows. Earnings are forecasted to grow 21.44% annually, outpacing the Hong Kong market's 11.7%, though revenue growth at 13.3% is slower than desired but still exceeds market averages. Despite a low projected return on equity of 8.5%, the company's undervaluation offers an attractive opportunity for investors focused on cash flow metrics.

- Our growth report here indicates Smoore International Holdings may be poised for an improving outlook.

- Click here and access our complete balance sheet health report to understand the dynamics of Smoore International Holdings.

DeHua TB New Decoration MaterialLtd (SZSE:002043)

Overview: DeHua TB New Decoration Material Co., Ltd specializes in the production and sale of environmentally friendly furniture panels both in China and internationally, with a market cap of CN¥9.22 billion.

Operations: Revenue Segments (in millions of CN¥): The company generates revenue through the production and sale of eco-friendly furniture panels in both domestic and international markets.

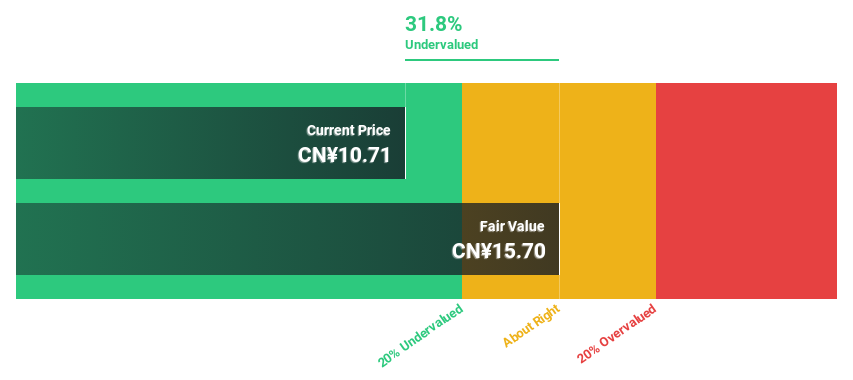

Estimated Discount To Fair Value: 29.6%

DeHua TB New Decoration Material Ltd., trading at CN¥11.22, is priced below its estimated fair value of CN¥15.94, offering an attractive opportunity for cash flow-focused investors. Earnings are projected to grow 22.28% annually, though slightly below the Chinese market's 25.5%. Recent earnings showed a decline in net income to CN¥588.27 million from the previous year's CN¥689.42 million, highlighting potential challenges despite its undervaluation and solid revenue growth forecasts of 13.6% per year.

- Our comprehensive growth report raises the possibility that DeHua TB New Decoration MaterialLtd is poised for substantial financial growth.

- Delve into the full analysis health report here for a deeper understanding of DeHua TB New Decoration MaterialLtd.

Taking Advantage

- Delve into our full catalog of 284 Undervalued Asian Stocks Based On Cash Flows here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com