What trends should we look for it we want to identify stocks that can multiply in value over the long term? Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. With that in mind, we've noticed some promising trends at EPI (Holdings) (HKG:689) so let's look a bit deeper.

What Is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. To calculate this metric for EPI (Holdings), this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.045 = HK$19m ÷ (HK$437m - HK$5.9m) (Based on the trailing twelve months to June 2024).

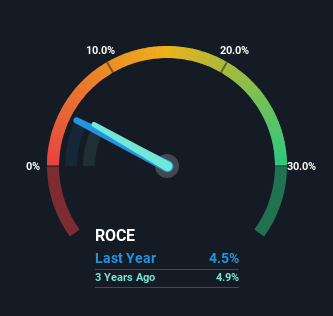

Thus, EPI (Holdings) has an ROCE of 4.5%. Ultimately, that's a low return and it under-performs the Oil and Gas industry average of 6.9%.

Check out our latest analysis for EPI (Holdings)

Historical performance is a great place to start when researching a stock so above you can see the gauge for EPI (Holdings)'s ROCE against it's prior returns. If you want to delve into the historical earnings , check out these free graphs detailing revenue and cash flow performance of EPI (Holdings).

So How Is EPI (Holdings)'s ROCE Trending?

We're delighted to see that EPI (Holdings) is reaping rewards from its investments and has now broken into profitability. Historically the company was generating losses but as we can see from the latest figures referenced above, they're now earning 4.5% on their capital employed. At first glance, it seems the business is getting more proficient at generating returns, because over the same period, the amount of capital employed has reduced by 21%. EPI (Holdings) could be selling under-performing assets since the ROCE is improving.

What We Can Learn From EPI (Holdings)'s ROCE

From what we've seen above, EPI (Holdings) has managed to increase it's returns on capital all the while reducing it's capital base. However the stock is down a substantial 77% in the last five years so there could be other areas of the business hurting its prospects. In any case, we believe the economic trends of this company are positive and looking into the stock further could prove rewarding.

Like most companies, EPI (Holdings) does come with some risks, and we've found 3 warning signs that you should be aware of.

While EPI (Holdings) may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.