Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Shandong Xinhua Pharmaceutical Company Limited (HKG:719) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Shandong Xinhua Pharmaceutical

What Is Shandong Xinhua Pharmaceutical's Net Debt?

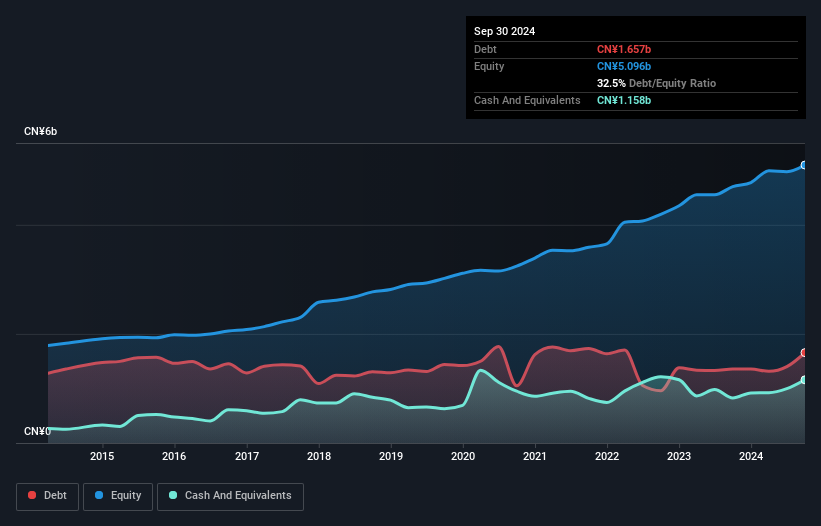

As you can see below, at the end of September 2024, Shandong Xinhua Pharmaceutical had CN¥1.66b of debt, up from CN¥1.35b a year ago. Click the image for more detail. However, because it has a cash reserve of CN¥1.16b, its net debt is less, at about CN¥498.4m.

How Healthy Is Shandong Xinhua Pharmaceutical's Balance Sheet?

According to the last reported balance sheet, Shandong Xinhua Pharmaceutical had liabilities of CN¥2.70b due within 12 months, and liabilities of CN¥1.02b due beyond 12 months. Offsetting this, it had CN¥1.16b in cash and CN¥1.10b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥1.47b.

Of course, Shandong Xinhua Pharmaceutical has a market capitalization of CN¥8.30b, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Shandong Xinhua Pharmaceutical's net debt is only 0.50 times its EBITDA. And its EBIT easily covers its interest expense, being 26.0 times the size. So we're pretty relaxed about its super-conservative use of debt. But the bad news is that Shandong Xinhua Pharmaceutical has seen its EBIT plunge 17% in the last twelve months. We think hat kind of performance, if repeated frequently, could well lead to difficulties for the stock. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Shandong Xinhua Pharmaceutical will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. Looking at the most recent three years, Shandong Xinhua Pharmaceutical recorded free cash flow of 37% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Our View

Shandong Xinhua Pharmaceutical's interest cover was a real positive on this analysis, as was its net debt to EBITDA. But truth be told its EBIT growth rate had us nibbling our nails. When we consider all the factors mentioned above, we do feel a bit cautious about Shandong Xinhua Pharmaceutical's use of debt. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. Over time, share prices tend to follow earnings per share, so if you're interested in Shandong Xinhua Pharmaceutical, you may well want to click here to check an interactive graph of its earnings per share history.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.