As global markets navigate the complexities of policy shifts under the new Trump administration, investors are witnessing fluctuations across various sectors, with notable impacts on financials and energy due to deregulation hopes, while healthcare faces challenges. Amidst this backdrop of economic uncertainty and shifting interest rates, small-cap stocks present unique opportunities for investors seeking growth potential in less-explored areas. In this environment, a good stock is often characterized by its resilience to market volatility and its ability to capitalize on emerging trends or regulatory changes.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| SALUS Ljubljana d. d | NA | 13.11% | 9.95% | ★★★★★★ |

| Parker Drilling | 46.25% | -0.33% | 53.04% | ★★★★★★ |

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Indo Tech Transformers | 1.82% | 23.43% | 58.49% | ★★★★★☆ |

| Magadh Sugar & Energy | 50.50% | 6.14% | 14.35% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

Here's a peek at a few of the choices from the screener.

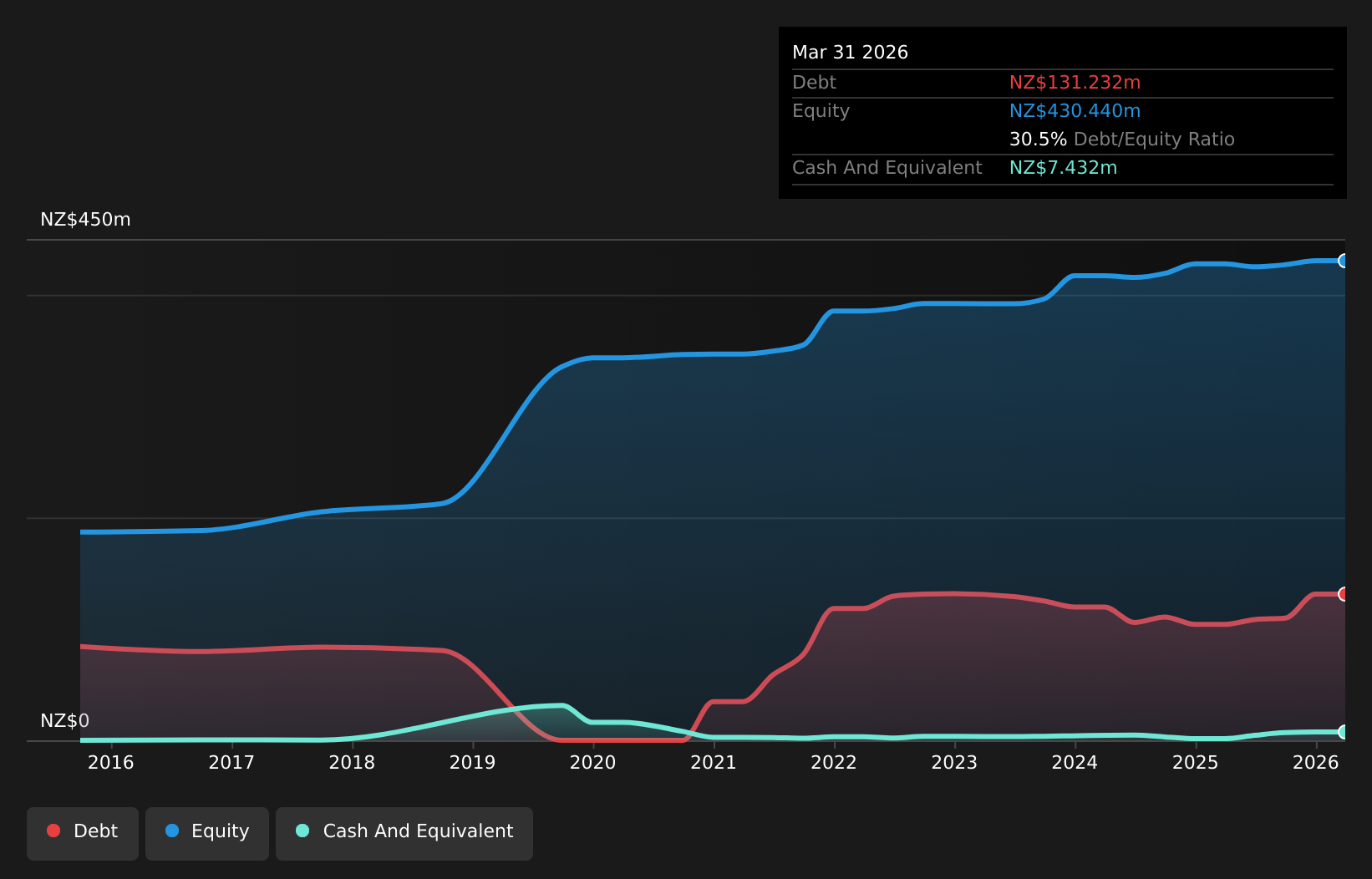

Napier Port Holdings (NZSE:NPH)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Napier Port Holdings Limited operates as a provider of various port services in New Zealand, with a market capitalization of NZ$504.57 million.

Operations: Napier Port Holdings generates revenue primarily through its port services in New Zealand. The company has a market capitalization of NZ$504.57 million, reflecting its scale in the industry.

Napier Port Holdings, a notable player in the infrastructure sector, showcases robust financial health with earnings growth of 49.7% over the past year, outpacing its industry peers. The company's debt management appears prudent, with a net debt to equity ratio at 26%, considered satisfactory and interest payments are well covered by EBIT at 5.8 times coverage. Recent annual results reveal sales climbed to NZ$141.35 million from NZ$121.95 million last year, while net income rose to NZ$24.83 million from NZ$16.59 million previously—marking significant strides in profitability and highlighting its potential as an investment opportunity.

- Navigate through the intricacies of Napier Port Holdings with our comprehensive health report here.

Evaluate Napier Port Holdings' historical performance by accessing our past performance report.

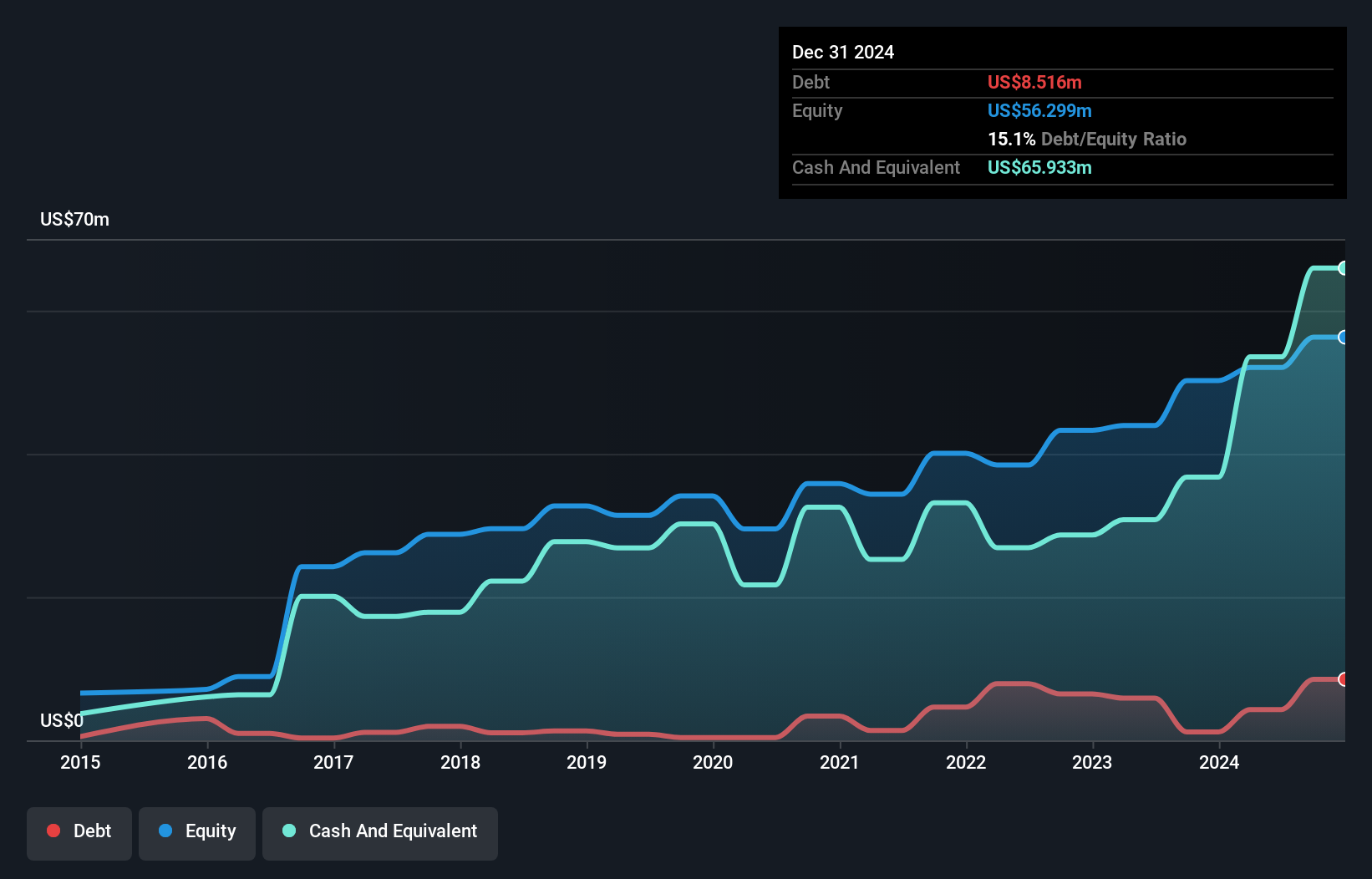

Plover Bay Technologies (SEHK:1523)

Simply Wall St Value Rating: ★★★★★☆

Overview: Plover Bay Technologies Limited is an investment holding company that designs, develops, and markets software-defined wide area network routers, with a market capitalization of HK$5.45 billion.

Operations: Plover Bay Technologies generates revenue through the sale of SD-WAN routers, with mobile-first connectivity contributing $59.87 million and fixed-first connectivity adding $15.19 million. Additionally, software licenses and warranty and support services account for $31.86 million in revenue.

Plover Bay Technologies, a nimble player in the tech field, has shown impressive financial health with earnings surging 41% over the past year. The company is trading at nearly half its estimated fair value, suggesting potential upside for investors. Its debt-to-equity ratio rose from 2.7 to 8.3 over five years but remains manageable given that cash exceeds total debt. Recent guidance indicates net profit for ten months ending October 2024 surpassed last year's figure by at least 10%, driven by increased SD-WAN router sales and new product contributions, alongside an improved net profit margin enhancing overall profitability.

- Get an in-depth perspective on Plover Bay Technologies' performance by reading our health report here.

Explore historical data to track Plover Bay Technologies' performance over time in our Past section.

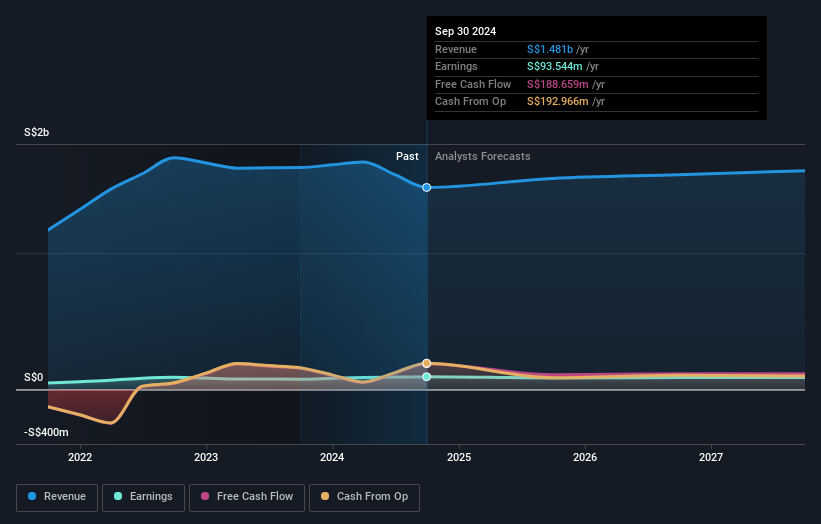

BRC Asia (SGX:BEC)

Simply Wall St Value Rating: ★★★★★★

Overview: BRC Asia Limited, with a market cap of SGD655.70 million, specializes in the prefabrication of steel reinforcement for concrete across various countries including Singapore, Australia, and several others internationally.

Operations: BRC Asia generates revenue through the prefabrication of steel reinforcement for concrete, operating in multiple international markets including Singapore and Australia. The company experienced a net profit margin of 9.5% in its recent financial period.

BRC Asia, a smaller player in the construction materials sector, has shown promising financial resilience. Over the past year, earnings rose to S$93.54 million from S$75.75 million, with basic earnings per share climbing to S$0.341 from S$0.2761. Despite a dip in sales to S$1.48 billion from last year's S$1.63 billion, their debt-to-equity ratio improved significantly over five years, dropping from 125% to 52%. This aligns with their satisfactory net debt-to-equity ratio of 11%. While revenue is expected to grow by 5% annually, future earnings may face challenges with a projected annual decline of 6%.

- Dive into the specifics of BRC Asia here with our thorough health report.

Assess BRC Asia's past performance with our detailed historical performance reports.

Where To Now?

- Access the full spectrum of 4627 Undiscovered Gems With Strong Fundamentals by clicking on this link.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com