As global markets experience varied shifts, the Hong Kong market has seen its benchmark Hang Seng Index decline by 2.11%, reflecting broader economic pressures and investor sentiment. In this environment, small-cap stocks in Hong Kong are drawing attention for their potential value, particularly those with significant insider buying activity, which can indicate confidence in a company's prospects amidst current market conditions.

Top 10 Undervalued Small Caps With Insider Buying In Hong Kong

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

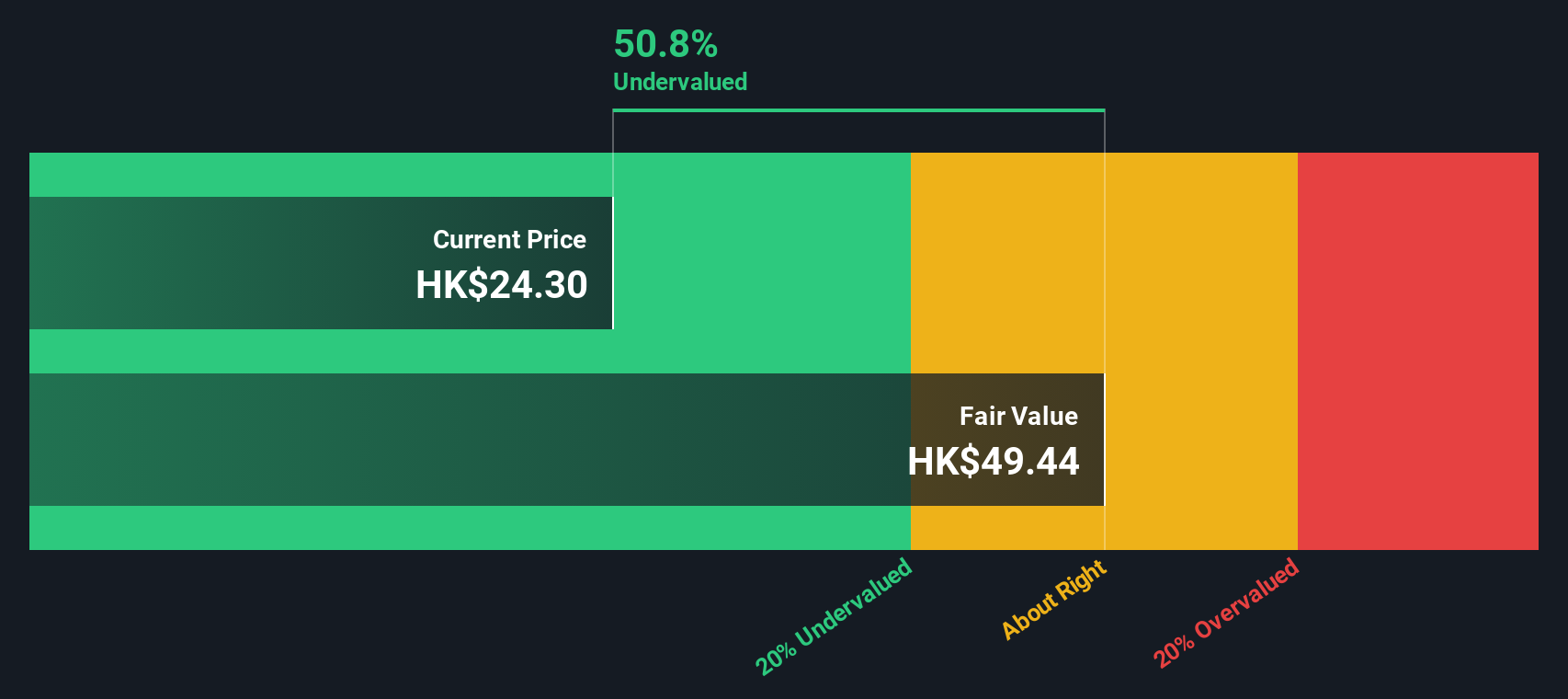

| Ferretti | 11.6x | 0.8x | 43.89% | ★★★★★☆ |

| Edianyun | NA | 0.6x | 41.04% | ★★★★★☆ |

| Vesync | 7.1x | 1.1x | -2.28% | ★★★★☆☆ |

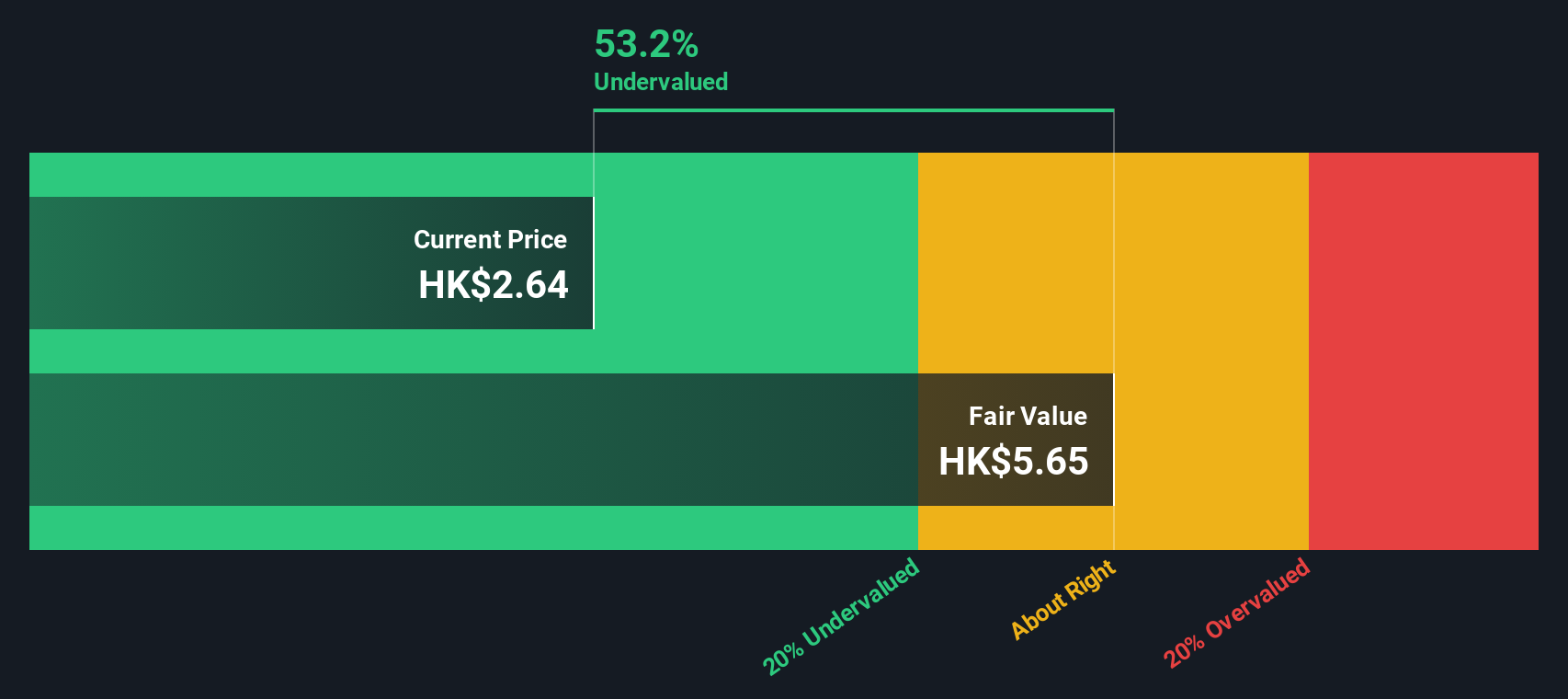

| Lion Rock Group | 5.5x | 0.4x | 49.29% | ★★★★☆☆ |

| Cheerwin Group | 11.1x | 1.4x | 47.53% | ★★★★☆☆ |

| Gemdale Properties and Investment | NA | 0.2x | 45.85% | ★★★★☆☆ |

| China Lesso Group Holdings | 5.7x | 0.4x | -495.82% | ★★★☆☆☆ |

| Skyworth Group | 5.6x | 0.1x | -291.96% | ★★★☆☆☆ |

| Lee & Man Paper Manufacturing | 7.1x | 0.4x | -44.56% | ★★★☆☆☆ |

| Emperor International Holdings | NA | 0.9x | 26.84% | ★★★☆☆☆ |

Let's explore several standout options from the results in the screener.

Vesync (SEHK:2148)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Vesync is a company that specializes in the design and manufacture of small home appliances and tools, with a market capitalization of approximately HK$2.5 billion.

Operations: The company generates revenue primarily from its Appliance & Tool segment, with recent figures reaching $604.75 million. The gross profit margin has shown an upward trend, reaching 48.46% as of the latest reporting period. Operating expenses are significant, with sales and marketing being a major component at $97.52 million in the most recent quarter.

PE: 7.1x

Vesync, a smaller player in Hong Kong's market, demonstrates potential value with recent insider confidence. Zhaojun Chen purchased 200,000 shares for approximately HK$828,979 in September 2024. The company reported a sales increase of US$296 million for the first half of 2024, up from US$277 million the previous year. Despite relying on external borrowing for funding, Vesync's inclusion in the S&P Global BMI Index and projected earnings growth suggest promising prospects ahead.

- Dive into the specifics of Vesync here with our thorough valuation report.

Assess Vesync's past performance with our detailed historical performance reports.

Cheerwin Group (SEHK:6601)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Cheerwin Group is a consumer goods company primarily engaged in the production and sale of household care, personal care, and pet products.

Operations: The company's primary revenue stream is derived from Household Care, with significant contributions from Pets and Pet Products and Personal Care. Over recent periods, the gross profit margin has shown an upward trend, reaching 47.89% as of the latest data point. Operating expenses are largely driven by sales and marketing efforts, followed by general and administrative costs.

PE: 11.1x

Cheerwin Group, a player in the consumer goods sector, has shown promising financial growth with sales climbing to CNY 1.25 billion for the first half of 2024 from CNY 1.13 billion last year, alongside an increase in net income to CNY 179 million. Insider confidence is evident as Danxia Chen acquired 300,000 shares recently. Despite relying solely on external borrowing for funding, Cheerwin's earnings are projected to grow annually by nearly 4%. The company also declared an interim dividend of RMB 0.0538 per share for this period, reflecting its commitment to returning value to shareholders amidst executive changes and strategic developments within its board structure.

- Navigate through the intricacies of Cheerwin Group with our comprehensive valuation report here.

Understand Cheerwin Group's track record by examining our Past report.

Ferretti (SEHK:9638)

Simply Wall St Value Rating: ★★★★★☆

Overview: Ferretti is engaged in the design, construction, and marketing of yachts and recreational boats, with a market capitalization of approximately HK$9.89 billion.

Operations: The company generates revenue primarily from the design, construction, and marketing of yachts and recreational boats. As of the latest period, it reported a gross profit margin of 36.04%. Operating expenses include significant allocations to general and administrative costs.

PE: 11.6x

Ferretti, a Hong Kong-listed company, has experienced significant changes recently. Despite being dropped from the S&P Global BMI Index in September 2024, insider confidence remains strong with share purchases indicating belief in future growth. The company's earnings for the first half of 2024 showed an increase to €695 million in sales and €43.9 million net income compared to the previous year. Leadership transitions include Mr. Jiang Kui's appointment as Chairman on August 29, 2024, suggesting strategic shifts ahead while maintaining stability during these changes.

- Click here and access our complete valuation analysis report to understand the dynamics of Ferretti.

Gain insights into Ferretti's past trends and performance with our Past report.

Seize The Opportunity

- Discover the full array of 11 Undervalued SEHK Small Caps With Insider Buying right here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com