Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Chinese Estates Holdings Limited (HKG:127) does use debt in its business. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Chinese Estates Holdings

What Is Chinese Estates Holdings's Debt?

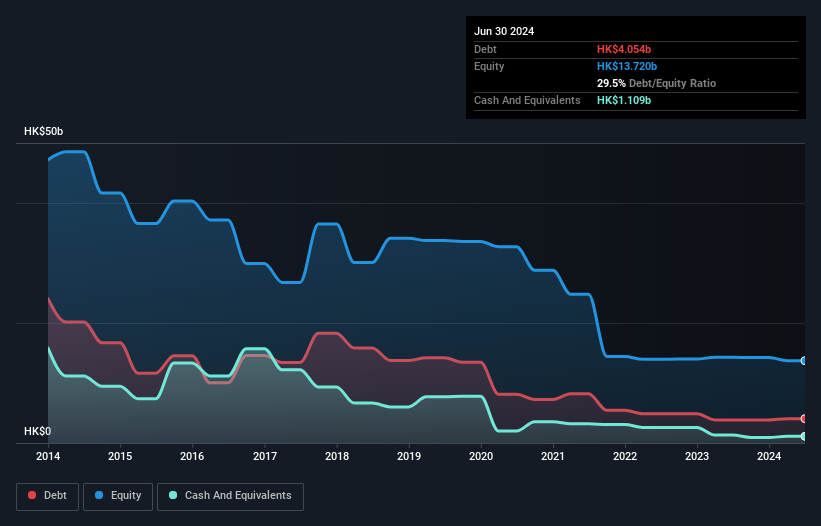

You can click the graphic below for the historical numbers, but it shows that as of June 2024 Chinese Estates Holdings had HK$4.05b of debt, an increase on HK$3.85b, over one year. On the flip side, it has HK$1.11b in cash leading to net debt of about HK$2.95b.

How Strong Is Chinese Estates Holdings' Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Chinese Estates Holdings had liabilities of HK$2.68b due within 12 months and liabilities of HK$1.79b due beyond that. On the other hand, it had cash of HK$1.11b and HK$161.9m worth of receivables due within a year. So it has liabilities totalling HK$3.20b more than its cash and near-term receivables, combined.

Given this deficit is actually higher than the company's market capitalization of HK$2.59b, we think shareholders really should watch Chinese Estates Holdings's debt levels, like a parent watching their child ride a bike for the first time. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Chinese Estates Holdings shareholders face the double whammy of a high net debt to EBITDA ratio (8.8), and fairly weak interest coverage, since EBIT is just 1.2 times the interest expense. This means we'd consider it to have a heavy debt load. Looking on the bright side, Chinese Estates Holdings boosted its EBIT by a silky 77% in the last year. Like the milk of human kindness that sort of growth increases resilience, making the company more capable of managing debt. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Chinese Estates Holdings will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Chinese Estates Holdings actually produced more free cash flow than EBIT. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Our View

While Chinese Estates Holdings's interest cover has us nervous. For example, its conversion of EBIT to free cash flow and EBIT growth rate give us some confidence in its ability to manage its debt. We think that Chinese Estates Holdings's debt does make it a bit risky, after considering the aforementioned data points together. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 1 warning sign for Chinese Estates Holdings that you should be aware of.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.