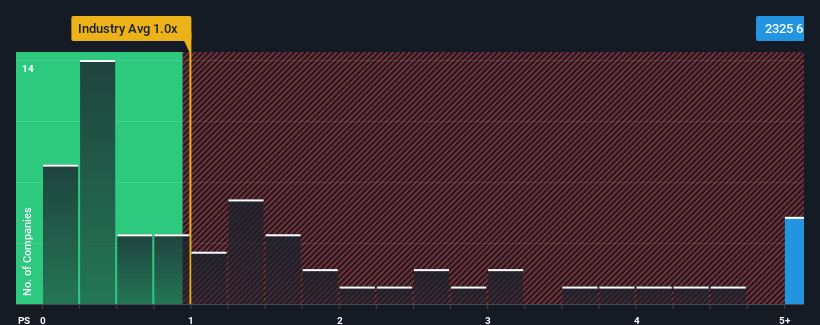

When close to half the companies in the Healthcare industry in Hong Kong have price-to-sales ratios (or "P/S") below 1x, you may consider Yunkang Group Limited (HKG:2325) as a stock to avoid entirely with its 6.2x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

See our latest analysis for Yunkang Group

How Has Yunkang Group Performed Recently?

While the industry has experienced revenue growth lately, Yunkang Group's revenue has gone into reverse gear, which is not great. It might be that many expect the dour revenue performance to recover substantially, which has kept the P/S from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Keen to find out how analysts think Yunkang Group's future stacks up against the industry? In that case, our free report is a great place to start.How Is Yunkang Group's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as steep as Yunkang Group's is when the company's growth is on track to outshine the industry decidedly.

Retrospectively, the last year delivered a frustrating 76% decrease to the company's top line. The last three years don't look nice either as the company has shrunk revenue by 26% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Turning to the outlook, the next three years should generate growth of 12% per year as estimated by the three analysts watching the company. With the industry predicted to deliver 14% growth per annum, the company is positioned for a weaker revenue result.

With this in consideration, we believe it doesn't make sense that Yunkang Group's P/S is outpacing its industry peers. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

The Bottom Line On Yunkang Group's P/S

It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've concluded that Yunkang Group currently trades on a much higher than expected P/S since its forecast growth is lower than the wider industry. When we see a weak revenue outlook, we suspect the share price faces a much greater risk of declining, bringing back down the P/S figures. At these price levels, investors should remain cautious, particularly if things don't improve.

The company's balance sheet is another key area for risk analysis. Our free balance sheet analysis for Yunkang Group with six simple checks will allow you to discover any risks that could be an issue.

If you're unsure about the strength of Yunkang Group's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com