The Main Investment Areas

Financial advisers are often asked, 'Where is the best place to invest my money?' In asking such a question, their clients are hoping to be told that there is one sure bet - that shares are better than property or government bonds are the best way to increase their wealth.

Of course, depending on your personal financial goals and objectives, one particular form of investment may be better than another for a period of time. However, it is never advisable to have all your eggs in one basket. Even the so - called safe investments such as bank savings accounts involve an element of risk, most notably the risk of their value being eroded by inflation.

There are different asset classes that each have a valid place in a diversified investment portfolio. By spreading your investments between different asset classes you are aiming to spread your investment risk and therefore smooth out your returns.

There are four main investment areas:

1. Cash - through which you invest money in a bank, building society, or other financial institution. Investment options include cash management accounts. The major benefit of this investment type is liquidity ('liquidity' refers to the ability to convert an investment into cash).

2. Fixed interest - through which you invest in short or long term interest rate products that provide a steady income stream. Investment options include bonds, hybrid securities, term deposits, and other types of securities.

3. Property - through which you invest in residential, rural, industrial or commercial property. Your own home may be included in this investment class, depending on your retirement plans and financial objectives.

4. Shares - through which you invest in companies listed on ASX and overseas stock exchanges.

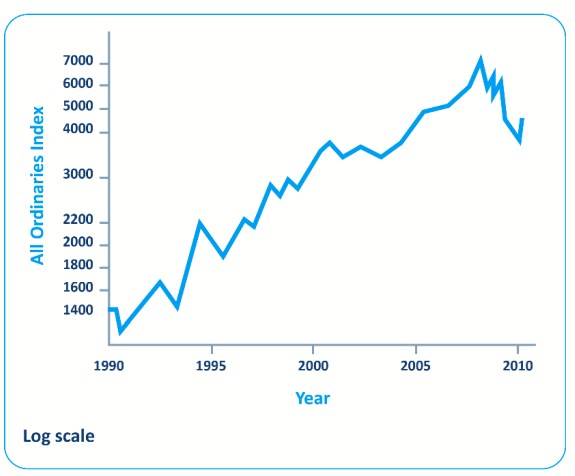

Comparing the performance of the main investment areas:

History demonstrates that shares, as a long - term investment, have the potential to provide strong returns when compared to other major investments.

Share values have historically risen over the long -term, but this has been punctuated with periods of short -term volatility, where prices can go up or down very quickly. Many financial advisers recommend a long term view when investing in the sharemarket – between 3 -7 years.

There is a lot of merit in the saying - 'past performance is not a guarantee of future returns.' Investors should keep this in mind when reviewing information on past investment performance figures.

Asset allocation

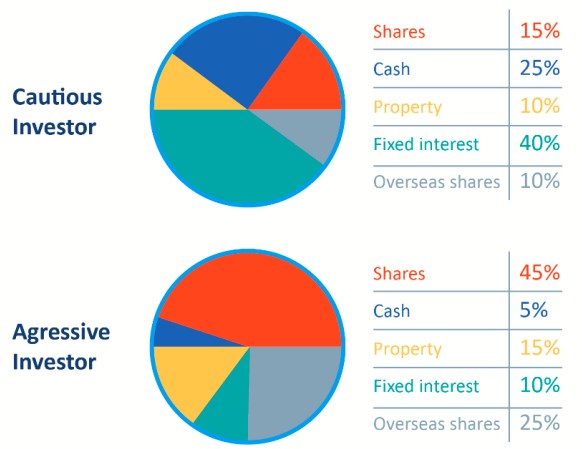

Within your investment strategy you need to work out what proportion of your total capital you should invest in shares, property, fixed interest and cash. This is called asset allocation.

Each sector should be weighted in accordance with economic conditions and investment prospects. This helps to reduce volatility and risk in your portfolio. Of equal importance is the need to achieve a balance between income and growth. Three common investor attitudes are:

Cautious investors seek better than basic returns, but insist that the risk must still be low. They seek to protect wealth that they have accumulated.

The prudent investor wants a balanced portfolio to work towards medium to long-term financial goals. They require an investment strategy that will cope with the effects of tax and inflation. Calculated risks aimed at achieving greater returns, in the form of both income and growth, are acceptable.

The aggressive investor is prepared to take greater risks in pursuit of potentially higher gains. They may take on a higher level of gearing and business risk.